- The Pound Sterling rebounded from seven-week lows against the US Dollar.

- GBP/USD recovery set to fade heading into the US inflation week.

- The Pound Sterling still targets 1.2400, as the daily RSI remains below 50.00.

The Pound Sterling (GBP) failed to sustain the bounce against the US Dollar (USD), as the GBP/USD pair lost upside momentum once again when it tried to reach 1.2700.

Pound Sterling tries another recovery attempt

GBP/USD broke its previous week’s consolidation to the downside and reached the lowest level in seven weeks near 1.2540 on Tuesday. The pair staged a rebound to hit a fresh two-week high shy of 1.2700 but buyers failed to sustain this momentum, pushing GBP/USD lower in the latter part of the week.

GBP/USD’s up and down price action was mainly driven by the sentiment surrounding the market’s pricing of a US Federal Reserve (Fed) dovish policy pivot as early as June. There was no significant fundamental catalyst from the United Kingdom (UK), and hence, the pair remained at the mercy of the US Dollar dynamics.

Earlier in the week, strong US ISM Manufacturing PMI, JOLTS Job Openings and ADP Employment Change data sponsored the rally in the US Dollar and the Treasury bond yields, anticipating that the Fed could delay its dovish policy pivot on the back of the US economic resilience.

“The ISM said on Monday that its manufacturing PMI increased to 50.3 last month, the highest and first reading above 50 since September 2022, from 47.8 in February. The rebound ended 16 straight months of contraction in manufacturing,” per Reuters. US job openings rose by 8,000 to 8.756 million on the last day of February, the Labor Department’s Bureau of Labor Statistics said on Tuesday. Meanwhile, the US private sector added 184,000 jobs in March, a decent increase from the upwardly revised 155,000 print in February, the ADP reported on Wednesday.

Despite strong data, markets continued to price in a 64% probability of a June Fed rate cut, according to the CME Group’s FedWatch Tool. This could be attributed to the recent commentaries from Fed officials.

Cleveland Fed President Loretta Mester said on Tuesday that she still expects interest rate cuts this year but ruled out the next policy meeting in May. San Francisco Fed President Mary Daly noted that three reductions this year is a “very reasonable baseline” though she said nothing is promised. Fed Chairman Jerome Powell on Wednesday reassured markets of the likelihood of interest rate cuts this year.

The Fedspeak likely triggered a sharp pullback in the US Treasury bond yields, prompting the US Dollar to turn south. However, a fresh bunch of Fed speakers on Thursday tempered Fed rate cut bets with their hawkish commentaries and propelled the Greenback while triggering a correction in the GBP/USD pair from two-week highs.

Chicago Fed President Austan Goolsbee said on Thursday that “if housing inflation does not come down, would be very difficult to return inflation to 2%”. Minneapolis Federal Reserve Bank President Neel Kashkari noted that “if inflation continues to move sideways, makes me wonder if we should cut rates at all this year”. Finally, Richmond Fed President Thomas Barkin said that “disinflation is likely to continue, but the speed of that remains unclear”. He added: “I think it is smart for the Fed to take our time.”

On Friday, the pair remained on the back foot amid broad risk-aversion, fuelled by intensifying geopolitical tensions between Israel and Iran. Later in the day, the Bureau of Labor Statistics reported that Nonfarm Payrolls (NFP) increased 303,000 in March, beating the market expectation of 200,000. Additionally, the Unemployment Rate edged lower to 3.8% from 3.9% in February. The USD gathered strength on the upbeat jobs report and caused GBP/USD to retreat below 1.2600 ahead of the weekend.

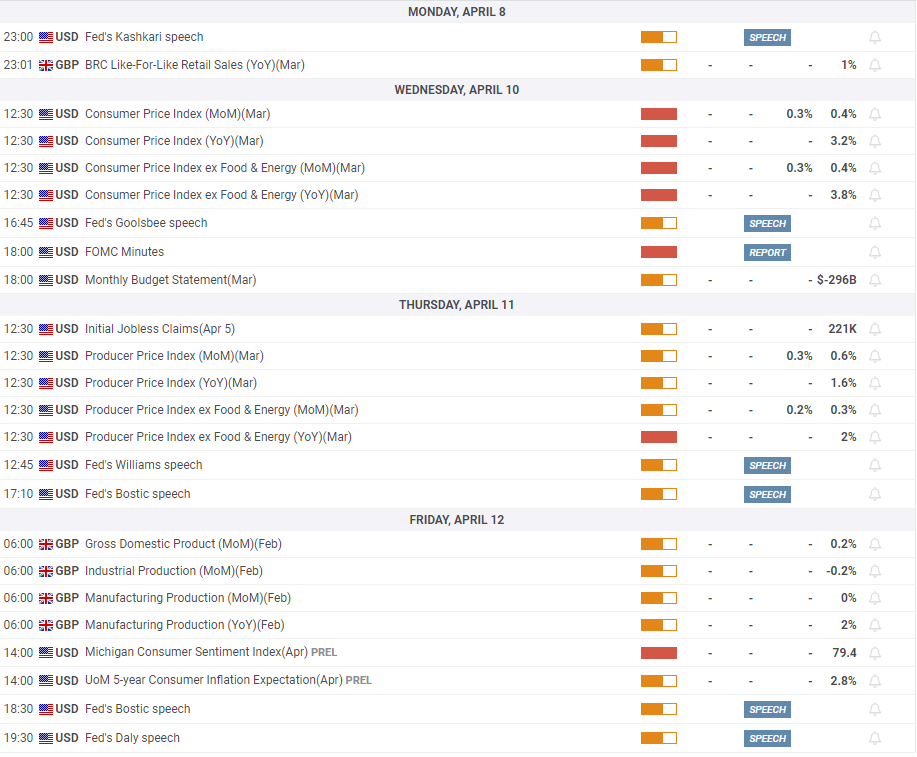

Week ahead: US CPI to hog the limelight

The US inflation data, the Consumer Price Index (CPI) on Wednesday and the Producer Price Index (PPI) on Thursday, are likely to stand in a relatively quiet week ahead.

Besides, the Minutes of the March Fed meeting, the UK monthly Gross Domestic Product (GDP) report for February and the US preliminary Michigan Consumer Sentiment and Inflation Expectations data will provide fresh trading impetus to GBP/USD.

Also of note will remain the speeches from Fed policymakers for gauging the timing and scope of the Fed interest rate cuts this year.

GBP/USD: Technical Outlook

From a short-term technical perspective, GBP/USD remains on track to extend the downside break from the rising channel seen a couple of weeks ago.

The bearish outlook could be based on the 14-day Relative Strength Index (RSI) indicator, which continues to stay below the midline near 46.00.

However, Pound Sterling sellers must settle the week below the horizontal 200-day Simple Moving Average (SMA) at 1.2587 for a sustained downtrend.

Sellers will then target the April low near 1.2540, followed by the 1.2500 round figure. Further south, the 1.2400 threshold could come to the rescue of buyers.

If buyers defend the 200-day SMA at 1.2587, it could alleviate the near-term selling pressure, allowing GBP/USD to attempt a comeback toward the static resistance shy of the 1.2700 level.

Inflation FAQs

Inflation measures the rise in the price of a representative basket of goods and services. Headline inflation is usually expressed as a percentage change on a month-on-month (MoM) and year-on-year (YoY) basis. Core inflation excludes more volatile elements such as food and fuel which can fluctuate because of geopolitical and seasonal factors. Core inflation is the figure economists focus on and is the level targeted by central banks, which are mandated to keep inflation at a manageable level, usually around 2%.

The Consumer Price Index (CPI) measures the change in prices of a basket of goods and services over a period of time. It is usually expressed as a percentage change on a month-on-month (MoM) and year-on-year (YoY) basis. Core CPI is the figure targeted by central banks as it excludes volatile food and fuel inputs. When Core CPI rises above 2% it usually results in higher interest rates and vice versa when it falls below 2%. Since higher interest rates are positive for a currency, higher inflation usually results in a stronger currency. The opposite is true when inflation falls.

Although it may seem counter-intuitive, high inflation in a country pushes up the value of its currency and vice versa for lower inflation. This is because the central bank will normally raise interest rates to combat the higher inflation, which attract more global capital inflows from investors looking for a lucrative place to park their money.

Formerly, Gold was the asset investors turned to in times of high inflation because it preserved its value, and whilst investors will often still buy Gold for its safe-haven properties in times of extreme market turmoil, this is not the case most of the time. This is because when inflation is high, central banks will put up interest rates to combat it. Higher interest rates are negative for Gold because they increase the opportunity-cost of holding Gold vis-a-vis an interest-bearing asset or placing the money in a cash deposit account. On the flipside, lower inflation tends to be positive for Gold as it brings interest rates down, making the bright metal a more viable investment alternative.