The highlight in the Australian economic docket this week is the April Consumer Price Index (CPI) figures, which are expected to be released by the Australian Bureau of Statistics (ABS) on Wednesday at 01:30 GMT. Consumer inflation is forecast to slow down to a 4.4% year-on-year (YoY) rate, down from 4.6% in March, yet still at its highest levels since 2023, and well above the Reserve Bank of Australia’s (RBA) 2% to 3% target for price stability.

The Australian government’s decision to halve fuel excise in April might have contributed to taming monthly inflation to 0.6% in April from the previous month’s 1.1% reading. The Trimmed Mean CPI, however, considered more relevant to assess underlying inflationary trends, is expected to have accelerated to 3.4% in the 12 months to April from 3.3% in March and 0.4% monthly from the previous 0.3% rate.

On the whole, these numbers might provide a momentary respite to the RBA, but they do not ease pressure on the central bank to keep tightening borrowing costs. Investors are pricing a pause at the next monetary policy meeting due in mid-June, as the consequences of Iran’s conflict seem to be starting to take a toll on the Australian economy.

What to expect from Australia’s inflation rate numbers?

April’s CPI figures are expected to confirm that the higher energy prices stemming from the Middle East conflict keep boosting consumer prices, although recent reports warn about pass-through effects, with inflationary effects visible on a range of products from food to recreation or building materials.

In this context, the central bank would celebrate some moderation on the CPI growth, especially after the labour data released last week showed that the Unemployment Rate unexpectedly rose to 4.5% in April, its highest level since September..

The RBA, nevertheless, remains focused on inflation as the main target of its monetary policy. The minutes of May’s meeting showed nearly unanimous support for the third consecutive interest rate hike and reflected a hawkishly-leaning stance as the board projects price pressures to remain above target for an extended period.

Analysts from Westpac support that view, as they see Australian inflation peaking at 5% this year, and return to the RBA’s target only in late 2027: “Brent oil is now expected to average $125 per barrel in Q2. Headline inflation is now expected to peak lower at 5.0%yr in Q3 2026, but prove more persistent, ending the year at 4.9%yr and reaching 2.5%yr by end-2027.”

Interest rates, however, are likely to remain steady at June’s meeting, with an August hike on the table. May’s minutes also revealed that most RBA board members consider the current 4.35% Cash Rate target as somewhat restrictive, and that there is now some margin to observe how households and businesses react to the current conditions and to developments in the Middle East. Any sign of inflation moderation, even a mild one, in this case, will support that stance.

How could the Consumer Price Index report affect AUD/USD?

With inflation figures well above target, and the US-Iran conflict in a stalemate, any deviation in the Consumer Price Index data might have a significant impact on the Australian Dollar’s volatility. April’s will be the last CPI release before the RBA’s June monetary policy meeting, and, although it is unlikely to alter expectations of a rate pause, it will provide further insight into the banks’ next steps.

If final numbers meet market consensus, the impact on the Aussie is expected to be minor, with all eyes on the US-Iran peace process. A lower-than-expected inflation will practically confirm steady interest rates in June, and might cast doubt on an August rate hike, which is highly likely to add bearish pressure on the Australian Dollar (AUD).

The risk, however, is of a strong CPI reading, especially if the yearly inflation accelerates unexpectedly. This would signal stronger-than-expected second-round inflationary effects and increase pressure on the RBA to keep tightening its monetary policy. This option would have a positive impact on the AUD.

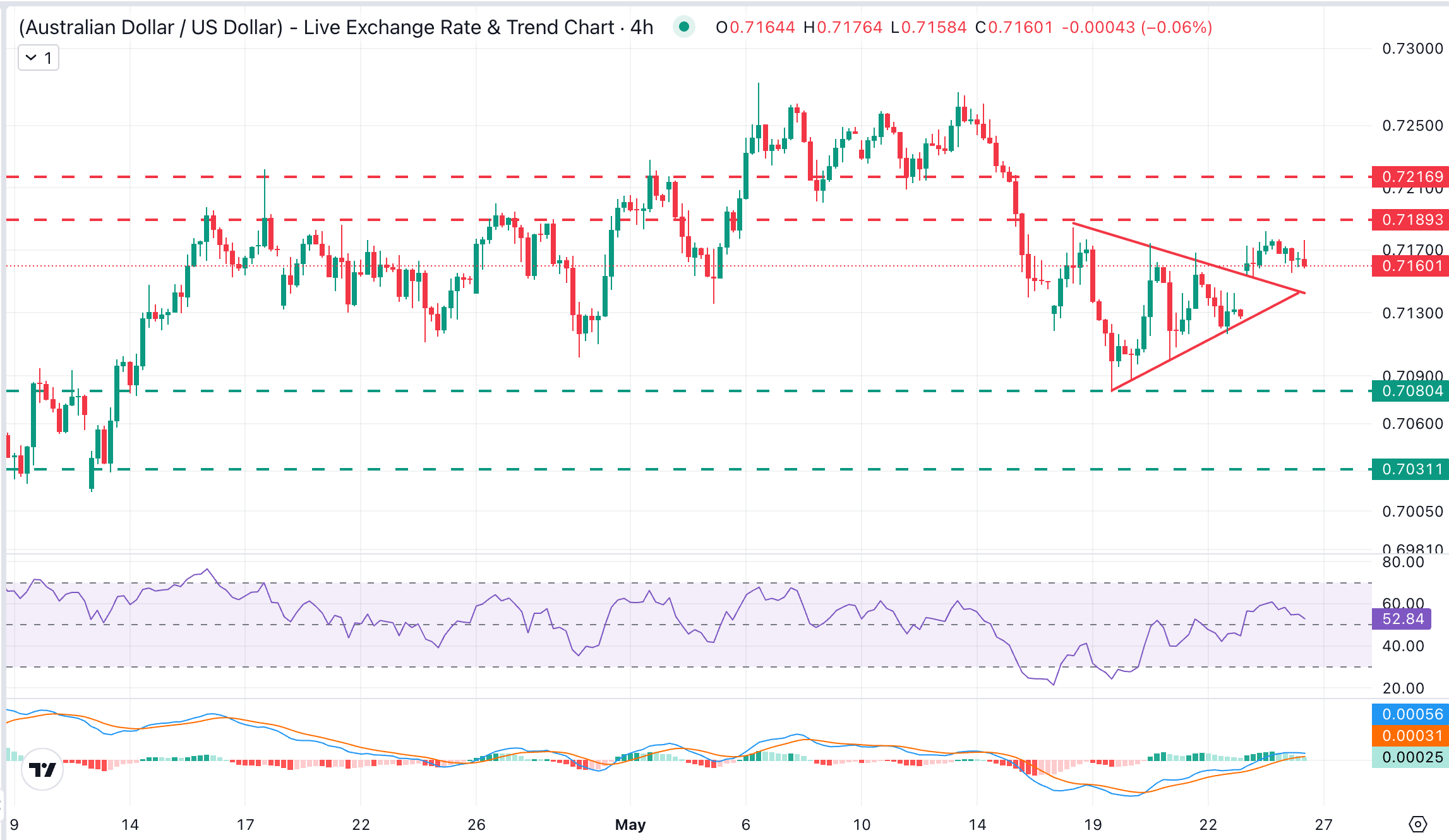

From a technical perspective, the AUD/USD is showing a somewhat stronger stance this week, according to FXStreet Analyst, Guillermo Alcala, although resistance around 0.7190 remains a significant hurdle for bulls: “The pair has broken above the triangle pattern observed last week, but bulls seem to be losing momentum after failing to breach resistance at the 0.7190 area.”

On the downside, Alcala sees key support at 0.7080: “Downside attempts are likely to find support at a reverse trendline, now in the area of 0.7145. Further down, a break of May’s 19 low at 0.7080 would signal the negation of the bullish view and expose the April 13 low, near 0.7030.”

Australian Dollar FAQs

One of the most significant factors for the Australian Dollar (AUD) is the level of interest rates set by the Reserve Bank of Australia (RBA). Because Australia is a resource-rich country another key driver is the price of its biggest export, Iron Ore. The health of the Chinese economy, its largest trading partner, is a factor, as well as inflation in Australia, its growth rate and Trade Balance. Market sentiment – whether investors are taking on more risky assets (risk-on) or seeking safe-havens (risk-off) – is also a factor, with risk-on positive for AUD.

The Reserve Bank of Australia (RBA) influences the Australian Dollar (AUD) by setting the level of interest rates that Australian banks can lend to each other. This influences the level of interest rates in the economy as a whole. The main goal of the RBA is to maintain a stable inflation rate of 2-3% by adjusting interest rates up or down. Relatively high interest rates compared to other major central banks support the AUD, and the opposite for relatively low. The RBA can also use quantitative easing and tightening to influence credit conditions, with the former AUD-negative and the latter AUD-positive.

China is Australia’s largest trading partner so the health of the Chinese economy is a major influence on the value of the Australian Dollar (AUD). When the Chinese economy is doing well it purchases more raw materials, goods and services from Australia, lifting demand for the AUD, and pushing up its value. The opposite is the case when the Chinese economy is not growing as fast as expected. Positive or negative surprises in Chinese growth data, therefore, often have a direct impact on the Australian Dollar and its pairs.

Iron Ore is Australia’s largest export, accounting for $118 billion a year according to data from 2021, with China as its primary destination. The price of Iron Ore, therefore, can be a driver of the Australian Dollar. Generally, if the price of Iron Ore rises, AUD also goes up, as aggregate demand for the currency increases. The opposite is the case if the price of Iron Ore falls. Higher Iron Ore prices also tend to result in a greater likelihood of a positive Trade Balance for Australia, which is also positive of the AUD.

The Trade Balance, which is the difference between what a country earns from its exports versus what it pays for its imports, is another factor that can influence the value of the Australian Dollar. If Australia produces highly sought after exports, then its currency will gain in value purely from the surplus demand created from foreign buyers seeking to purchase its exports versus what it spends to purchase imports. Therefore, a positive net Trade Balance strengthens the AUD, with the opposite effect if the Trade Balance is negative.