Welcome to Japan’s Groundhog Day: the Japanese Yen continues to severely underperform against major global currencies and remains close (again) to the 160.00 threshold against the US Dollar. Support from the Bank of Japan in the form of an interest rate hike on June 16 would certainly ease the pain, but it is unclear whether Japanese authorities can wait until then.

Recent interventions have provided short-term respite but failed to turn the tide, as they don’t address the root cause of the Yen’s weakness. Moreover, geopolitics and central bank policy factors put the Yen in danger of weakening further. Will Japan fire its Yen bazooka again?

The pressure on the JPY intensifies

The JPY has come under fierce selling pressure in the wake of economic concerns stemming from the Iran war. Japan imports over 90% of its crude Oil from the Middle East, leaving it highly vulnerable to supply chain disruptions caused by the closure of the Strait of Hormuz.

In fact, Japan relies on the strategic waterway for over 90% of its Crude Oil imports and a vast majority of the Liquefied Natural Gas (LNG). Bottlenecks impact Japanese factories directly, inflating raw material costs, exacerbating inflation, and squeezing consumer purchasing power.

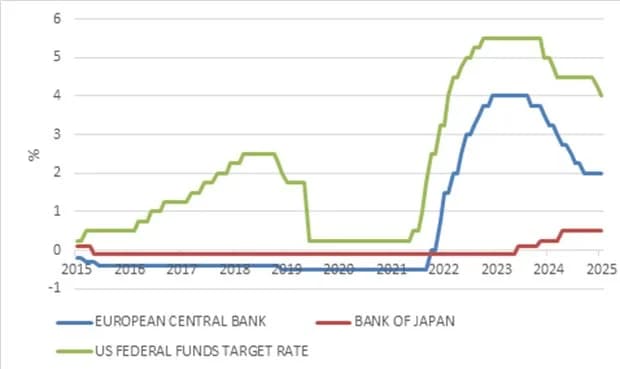

A widening rate gap contributes to the JPY fall

This puts the BoJ in a severe policy dilemma: raising interest rates amid the threat of inflation could dent a fragile economy, while holding rates down risks further currency depreciation.

In April, a rare vote split at the April BoJ meeting reflected growing pressure to increase interest rates in the near term. April’s discussions over the possibility of a hike, combined with the continued Yen weakness, make economists believe that the BoJ will indeed proceed to increase borrowing costs at its next meeting on June 16.

Still, it is unclear whether a hike will solve the Yen’s problems.

This is because the BoJ is still lagging other major central banks, which raised rates aggressively to combat inflation post-pandemic. This resulted in a massive interest rate gap that further contributed to the Yen’s weakness.

Government interventions fail to reverse the bearish trend

To prop up the embattled currency, Japanese authorities have spent a record ¥11.73 trillion ($74+ billion) in intervention between late April and early May.

The move, however, delivered only temporary relief for the Yen, as the aforementioned fundamental drivers continue to push the currency lower. Furthermore, Japan’s financial resources are finite, suggesting that the real pivot relies on the BoJ. Until then, the effect of any government intervention, even a potential joint action with the US, is unlikely to reverse the broader JPY bearish trend.

The Yen remains trapped between two forces Japan cannot easily control: high global energy prices and a wide interest-rate gap with other major central banks, particularly the Fed.

Another intervention in the Forex market could slow the move toward 160.00, but unless the BoJ delivers a stronger policy signal, any relief may prove short-lived. That leaves traders facing a familiar question: will Japan defend the line again?