The Bitcoin whitepaper, published by the pseudonymous Satoshi Nakamoto, marks its 17th anniversary on Friday. Over the past 17 years, BTC has evolved from a peer-to-peer digital cash concept to an institutional-grade asset class, backed by spot ETFs, corporate treasuries, and sovereign adoption.

EUR/USD Weekly Forecast: Is there life for the US Dollar after the Federal Reserve surprise?

The EUR/USD pair ended October with a weak note, barely holding above a three-month low of 1.1522 posted in the last trading day of the month. The pair is down for a second consecutive week following the Federal Reserve (Fed) and European Central Bank (ECB) monetary policy decisions.

Federal Reserve hawkish cut

The Federal Open Market Committee (FOMC) decided to trim the benchmark interest rate by 25 basis points (bps) to a range of 3.75% to 4%. There were two dissenters: Stephen Miran, who voted for a 50 bps cut, and Jeffrey Schmid, who preferred to keep rates unchanged. Policymakers also announced an end to the quantitative tightening (QT) program. The decision, alongside the statement, had a limited impact on financial markets, but things changed after Chair Jerome Powell delivered a press conference.

Chair Powell was pretty hawkish, noting that the decision to trim interest rates was risk management while adding that a December cut should not be taken for granted. The US Dollar (USD) soared and stocks edged firmly lower amid speculative interest rolling back bets for a December cut.

Additionally, Powell highlighted the challenges in assessing the economic situation amid the government shutdown, resulting in the absence of official data, particularly employment-related data. “There’s a possibility that it would make sense to be more cautious,” Powell noted, adding, “I’m not committing to that, I’m just saying it’s certainly a possibility that you would say, ‘we really can’t see, so let’s slow down.’”

European Central Bank on hold

The ECB announced its decision on monetary policy on Thursday, and as widely anticipated, European policymakers kept interest rates on hold. Therefore, the interest rate on the main refinancing operations, the interest rates on the marginal lending facility and the deposit facility stood at 2.15%, 2.4% and 2%, respectively. The decision came as no surprise, given that not only policymakers anticipated, but also that the loosening cycle had begun much earlier than the Fed. The ECB started trimming rates in June 2024 and delivered eight cuts that resulted in interest rates reaching a comfortable neutral rate, without any signs of increased price pressures and the economy posting modest yet steady growth.

President Christine Lagarde repeated that the ECB is in a good place during the press conference that followed the decision, also reiterating that officials stand ready to ensure that inflation stabilizes at its 2% target in the medium term. Finally, Lagarde mentioned that some of the downside risks to growth have abated, but that with inflation is not the same.

The ECB decision had no real impact on the Euro (EUR), with EUR/USD extending its weekly decline after market participants digested the news.

US government shutdown and trade war

Meanwhile, the US government shutdown has been ongoing for a month. The federal government ran out of funding on October 1, and the Senate has been unable to agree on a bill to reverse the situation. Financial markets have become more aware of the long-term effects after the Fed’s announcement, yet are still looking at the situation with a dose of calm.

Also, trade-war back-and-forth dominated headlines throughout the week. News from such a front was mostly positive after US President Donald Trump met with his Chinese counterpart, Xi Jinping, in South Korea. Both leaders announced a de-escalation of the latest measures, with the US reducing fentanyl-related tariffs to 10%, and China agreeing to buy more agricultural goods from the US. Beijing also suspended rare-earth export controls and agreed to explore energy sector cooperation.

The US also announced an enhanced trade agreement with Japan, a framework to coordinate on important minerals that reaffirmed their previous mutual commitments. US President Trump met with Prime Minister Sanae Takaichi on Tuesday, later announcing the US will charge 15% tariffs on Japanese goods, down from the initially threatened 25%, while Japan pledged to invest $550 billion in US industry and open its market to some American goods such as rice, cars, and defense equipment.

Mixed European data

Germany released data throughout the week, which came in mixed. The IFO Business Climate survey improved in October to 88.4 from 87.7 posted in September, yet Consumer Confidence deteriorated according to the GfK survey, which shrank to -24.1 in November from -22.3 previously.

The country also published the preliminary estimate of the Q3 Gross Domestic Product (GDP), which showed the economy did not grow in the three months to September. The reading was better than the -0.3% posted in Q2, but still discouraging. Finally, Germany released the preliminary estimate of the October Harmonized Index of Consumer Prices (HICP), which rose at an annualized pace of 2.3% as expected. The monthly HICP rose by 0.3%, slightly higher than the 0.2% posted in September.

As for the Eurozone, the Q3 GDP was up 0.2% QoQ, better than the previous 0.1%, while October Consumer Confidence printed at -14.2, matching September’s reading and expectations. Regarding the HICP, the preliminary October estimate printed at 2.1% YoY, easing from the previous 2.2%, while the core annual reading remained steady at 2.4%, higher than the 2.3% expected.

What’s next in the docket

The macroeconomic calendar will include the final estimates of the October S&P Global Manufacturing Purchasing Managers’ Indexes (PMIs) for both economies, and the official US ISM Manufacturing PMI on Monday.

Germany will publish September Factory Orders, while the Eurozone will unveil the Producer Price Index (PPI) for the same month on Wednesday. S&P Global will release the same day the Services and Composite PMIs for both economies, while the US will publish the October ADP Employment Change survey and the ISM Services PMI for the same month. Finally, the Eurozone will release September Retail Sales on Thursday.

A self-note goes for policymakers: multiple ECB and Fed officials will be on the wires throughout the week after the blackout periods ended with the monetary policy announcements.

EUR/USD technical outlook

In the daily chart, EUR/USD is currently trading at 1.1528. A bearish 20 SMA slides south below at 1.1622, while below a directionless 100 SMA at 1.1665. The 200 SMA, on the contrary, continues to advance below the current level, at 1.1314, underpinning the pair on dips. With spot holding below the 20- and 100-day SMAs, the path of least resistance remains to the downside.

In the same chart, the Momentum indicator remains in negative territory, indicating a waning but still present downward traction. At the same time, the RSI indicator continues to grind lower, reaching 36.5, which is well beneath the 50 mid-line and not yet oversold, reinforcing a bearish bias. As long as EUR/USD lingers beneath the falling 20-day average, sellers retain control; a recovery would first need to clear 1.1622 and then 1.1665 to alleviate pressure, while failure to do so risks another test of the advancing 200-day SMA at 1.1314.

In the weekly chart, EUR/USD is holding beneath a flattening 20-week SMA at 1.1674 but comfortably above the rising 100-week and 200-week SMAs at 1.1016 and 1.0836, respectively. The short-term average remains above the longer ones yet has lost directional strength, while the 100- and 200-week curves continue to advance, preserving a broader positive bias. The 20-week SMA caps the immediate topside as resistance, with dynamic support aligned first at the 100-week SMA, followed by the 200-week mark.

Oscillators echo this stalling tone: the Momentum indicator is marginally negative and oscillating around its midline, lacking traction, while the weekly RSI is flat around the 50 threshold, signaling a neutral stance. A decisive weekly close above 1.1674 is needed to re-energize the bullish narrative and open the door to additional gains; failure to clear that barrier would likely keep the pair range-bound and risk a gradual drift toward 1.1016, with 1.0836 as a deeper line of defense.

(This content was partially created with the help of an AI tool)

USD/CAD crawls above 1.4000 favoured by a hawkish Fed, risk-off markets

The US Dollar trades higher against its Canadian counterpart for the second consecutive day on Friday, returning to levels right above the 1.4000 psychological level to retrace losses from previous days, and trading practically flat on the weekly chart. The Hawkish comments by Federal Reserve (Fed) Chairman Jerome Powell and a. moderate risk aversion are buoying the Greenback against most of its main peers.

The US Dollar bounced from weekly lows at the 1.3890 area following the Fed’s monetary policy decision on Wednesday. The bank met expectations and trimmed its Federal Funds rate to a three-year low in the 3.75%-4% range, but Chairman Powell rattled markets, affirming that a December rate cut is far from a done deal, which sent US Treasury yields and the US Dollar higher.

Furthermore, the framework agreement between US President Trump and the Chinese Premier Xi Jinping has allowed to extension of the trade truce between the US and China. Trump has pledged to reduce tariffs on Chinese imports in exchange for keeping rare earth trade flowing and resuming purchases of US soybeans, which has provided additional support to the US Dollar.

Also on Wednesday, the Bank of Canada trimmed its benchmark interest rates by 25 basis points, to 2.25% and hinted at the end of the easing cycle, although Goverm¡nor Macklem kept all options open, assuring that the central bank will be ready to respond if Canada’s economic Outlook changed materially.

The Canadian Dollar bounced up following the BoC’s monetary policy decision, but has been losing ground over the last two days, weighed by a firmer US Dollar amid a moderate risk-off mood and falling Oil prices, Canada’s main export. The price of the West Texas Intermediate (WTI) barrel have dropped nearly 2% this week, to levels right above $60.00 at the time of writing, from last week’s highs near $62.50.

Canadian Dollar FAQs

The key factors driving the Canadian Dollar (CAD) are the level of interest rates set by the Bank of Canada (BoC), the price of Oil, Canada’s largest export, the health of its economy, inflation and the Trade Balance, which is the difference between the value of Canada’s exports versus its imports. Other factors include market sentiment – whether investors are taking on more risky assets (risk-on) or seeking safe-havens (risk-off) – with risk-on being CAD-positive. As its largest trading partner, the health of the US economy is also a key factor influencing the Canadian Dollar.

The Bank of Canada (BoC) has a significant influence on the Canadian Dollar by setting the level of interest rates that banks can lend to one another. This influences the level of interest rates for everyone. The main goal of the BoC is to maintain inflation at 1-3% by adjusting interest rates up or down. Relatively higher interest rates tend to be positive for the CAD. The Bank of Canada can also use quantitative easing and tightening to influence credit conditions, with the former CAD-negative and the latter CAD-positive.

The price of Oil is a key factor impacting the value of the Canadian Dollar. Petroleum is Canada’s biggest export, so Oil price tends to have an immediate impact on the CAD value. Generally, if Oil price rises CAD also goes up, as aggregate demand for the currency increases. The opposite is the case if the price of Oil falls. Higher Oil prices also tend to result in a greater likelihood of a positive Trade Balance, which is also supportive of the CAD.

While inflation had always traditionally been thought of as a negative factor for a currency since it lowers the value of money, the opposite has actually been the case in modern times with the relaxation of cross-border capital controls. Higher inflation tends to lead central banks to put up interest rates which attracts more capital inflows from global investors seeking a lucrative place to keep their money. This increases demand for the local currency, which in Canada’s case is the Canadian Dollar.

Macroeconomic data releases gauge the health of the economy and can have an impact on the Canadian Dollar. Indicators such as GDP, Manufacturing and Services PMIs, employment, and consumer sentiment surveys can all influence the direction of the CAD. A strong economy is good for the Canadian Dollar. Not only does it attract more foreign investment but it may encourage the Bank of Canada to put up interest rates, leading to a stronger currency. If economic data is weak, however, the CAD is likely to fall.

,

USD/INR gains as US Dollar trades firmly near almost three-month high

The Indian Rupee (INR) trades lower against the US Dollar (USD) after a flat opening on Friday. The USD/INR pair rises to near 88.90 as the US Dollar (USD) trades broadly firm due to receding Federal Reserve (Fed) dovish bets, and improving trade relations between the United States (US) and China.

At the press time, the US Dollar Index (DXY), which tracks the Greenback’s value against six major currencies, clings to gains near an almost three-month high around 99.70 posted on Thursday.

The CME FedWatch tool showed that the probability of the Fed cutting interest rates by 25 basis points (bps) to 3.50%-3.75% in the December meeting has eased to 72.8% from 91.1% seen a week ago. Fed dovish bets have cooled down after the monetary policy announcement on Wednesday, in which Chairman Jerome Powell argued against reducing interest rates in the December meeting after reducing them by 25 bps to 3.75%-4.00%. “Another cut in December is far from assured,” Powell said in the press conference.

For more cues on the interest rate outlook, investors await speeches from Federal Open Market Committee (FOMC) members: Atlanta President Raphael Bostic and Cleveland President Beth Hammack, scheduled during the North American session. Investors would also like to know the current status of the labor market amid the absence of economic data releases due to the ongoing federal shutdown.

Daily digest market movers: FIIs sell-off weigh on Indian Rupee

- Signs of improving trade relations between the US and China are also providing support to the USD/INR pair. On Thursday, US President Donald Trump stated that the “meeting with Chinese leader Xi Jinping was amazing”. Trump added, “On a scale of 1 to 10, the meeting with Xi was a 12”.

- Trump further added that tariffs on China will be 47%, down from 57% as Beijing is ready to cooperate on fentanyl issues, there will be no roadblocks on rare earth exports to Washington, and Beijing will begin purchasing soybeans soon.

- In response, the Chinese Commerce Ministry has stated that Beijing will suspend export control measures announced on October 9 for a year and will expand agricultural trade with Washington.

- Later on Thursday, US Treasury Secretary Scott Bessent stated in an interview on Fox Business Network that both Washington and Beijing would sign the trade deal soon. “The Kuala Lumpur agreement was finished in the middle of the night last night, so I expect we will exchange signatures possibly as soon as next week,” Bessent said, Reuters reported.

- In Asia, the Indian Rupee trades lower against its peers on renewed selling by overseas investors in the Indian stock market. This week, investors turned slightly optimistic on Foreign Institutional Investors (FIIs) returning to the Indian equity market after they bought shares worth Rs. 10,339.80 crores on Tuesday. However, the optimism has started fizzling out as FIIs have pared stake worth Rs. 5,617.75 crores cumulatively on Wednesday and Thursday.

- Going forward, more development on trade talks between the US and India will be a key trigger for the next move in the Indian Rupee. So far top negotiators from both nations have expressed confidence that they will reach a deal soon. However, no announcement has been made yet.

- Meanwhile, Indian equity markets are going through some volatility as the Q2 earnings season has picked up a little pace. So far, earnings from IT companies have remained tepid due to tariff uncertainty in the US economy.

The table below shows the percentage change of Indian Rupee (INR) against listed major currencies today. Indian Rupee was the weakest against the Japanese Yen.

| USD | EUR | GBP | JPY | CAD | AUD | INR | CHF | |

|---|---|---|---|---|---|---|---|---|

| USD | -0.06% | 0.00% | -0.09% | 0.06% | 0.20% | 0.09% | -0.02% | |

| EUR | 0.06% | 0.05% | -0.02% | 0.11% | 0.27% | 0.16% | 0.04% | |

| GBP | -0.00% | -0.05% | -0.10% | 0.06% | 0.21% | 0.11% | -0.03% | |

| JPY | 0.09% | 0.02% | 0.10% | 0.13% | 0.28% | 0.21% | 0.04% | |

| CAD | -0.06% | -0.11% | -0.06% | -0.13% | 0.14% | 0.06% | -0.08% | |

| AUD | -0.20% | -0.27% | -0.21% | -0.28% | -0.14% | -0.09% | -0.22% | |

| INR | -0.09% | -0.16% | -0.11% | -0.21% | -0.06% | 0.09% | -0.14% | |

| CHF | 0.02% | -0.04% | 0.03% | -0.04% | 0.08% | 0.22% | 0.14% |

The heat map shows percentage changes of major currencies against each other. The base currency is picked from the left column, while the quote currency is picked from the top row. For example, if you pick the Indian Rupee from the left column and move along the horizontal line to the US Dollar, the percentage change displayed in the box will represent INR (base)/USD (quote).

Technical Analysis: USD/INR stabilizes above 20-day EMA

-1761891126011-1761891126013.png&w=1536&q=95)

USD/INR rises to near 88.90 on Friday. The pair returns and strives to hold above the 20-day Exponential Moving Average (EMA), which trades around 88.49. This suggests that the near-term trend has become bullish.

The 14-day Relative Strength Index (RSI) strives to break above 60.00. A fresh bullish momentum would emerge if the RSI sustains above that level.

Looking down, the August 21 low of 87.07 will act as key support for the pair. On the upside, the all-time high of 89.12 will be a key barrier.

Economic Indicator

Fed Interest Rate Decision

The Federal Reserve (Fed) deliberates on monetary policy and makes a decision on interest rates at eight pre-scheduled meetings per year. It has two mandates: to keep inflation at 2%, and to maintain full employment. Its main tool for achieving this is by setting interest rates – both at which it lends to banks and banks lend to each other. If it decides to hike rates, the US Dollar (USD) tends to strengthen as it attracts more foreign capital inflows. If it cuts rates, it tends to weaken the USD as capital drains out to countries offering higher returns. If rates are left unchanged, attention turns to the tone of the Federal Open Market Committee (FOMC) statement, and whether it is hawkish (expectant of higher future interest rates), or dovish (expectant of lower future rates).

Last release: Wed Oct 29, 2025 18:00

Frequency: Irregular

Actual: 4%

Consensus: 4%

Previous: 4.25%

Source: Federal Reserve

AUD/USD remains near 0.6550 following China’s NBS PMI data

AUD/USD remains subdued for the third successive session, trading around 0.6550 during the Asian hours on Friday. The pair moves little following the release of China’s NBS Purchasing Managers’ Index (PMI) data. It is important to note that any shift in China’s economic conditions could also affect the Australian dollar (AUD), given the close trade ties between China and Australia.

China’s NBS Manufacturing Purchasing Managers’ Index dropped sharply to 49.0 in October, following 49.8 recorded in September. The reading came in above the expected 49.6 figure in the reported month. Meanwhile, the NBS Non-Manufacturing PMI unexpectedly rose slightly to 50.1 against the previous and the market consensus of 50.0 readings.

The AUD/USD pair faced challenges as the Australian Dollar (AUD) struggled amid market sentiment that remained subdued following the meeting between Presidents Donald Trump and Xi Jinping, which offered few positive surprises. President Trump announced that tariffs on China would be reduced to 47% from the current 57% and confirmed that the rare earth dispute had been resolved, removing restrictions on China’s rare earth exports. However, Trump acknowledged that not all matters were addressed during the talks.

The Federal Reserve lowered its benchmark rate by 25 basis points to a range of 3.75%–4% in a 10–2 vote. The decision was not unanimous, as Fed Governor Stephen Miran supported a larger 50-basis-point cut, while Kansas City Fed President Jeffrey Schmid voted to keep rates unchanged.

Fed Chair Jerome Powell stated that the available data indicate little change in the outlook for employment and inflation since the September meeting. Powell added that another rate cut in December is far from certain, emphasizing that the path forward remains uncertain, which provided support for the US Dollar (USD).

Economic Indicator

NBS Manufacturing PMI

The NBS Manufacturing Purchasing Managers Index (PMI), released by the China Federation of Logistics & Purchasing (CFLP) and China’s National Bureau of Statistics (NBS), is a leading indicator gauging business activity in China’s manufacturing sector. The data is derived from surveys of senior executives at manufacturing companies. Survey responses reflect the change, if any, in the current month compared to the previous month and can anticipate changing trends in official data series such as Gross Domestic Product (GDP), industrial production, employment and inflation. The index varies between 0 and 100, with levels of 50.0 signaling no change over the previous month. A reading above 50 indicates that the manufacturing economy is generally expanding, a bullish sign for the Renminbi (CNY). Meanwhile, a reading below 50 signals that activity among goods producers is generally declining, which is seen as bearish for CNY.

EUR/USD sinks below 1.16 as Fed’s hawkish cut and ECB hold weigh on Euro

EUR/USD retreats on Thursday as the European Central Bank (ECB) decided to hold rates unchanged, but traders, still digesting the ‘hawkish’ cut by the Federal Reserve (Fed) on Wednesday, kept the shared currency below the 1.1600 figure. The pair trades at 1.1565, down 0.30%.

ECB’s Lagarde says policy is “in a good place” as risks ease

The ECB kept its three interest rates unchanged, with the Deposit Facility, Main Refinancing and Marginal Lending Rates holding steady at 2.00%, 2.15%, and 2.40%, respectively. ECB’s President Christine Lagarde noted that monetary policy is in a “good place” as economic risks diminish and the economy in the Eurozone (EZ) shows signs of resilience.

Lagarde added that the Europe-US trade, the Middle East war de-escalation and the trade truce between China and the US had mitigated downside risks to growth.

The ECB is expected to publish its economic projections through 2028 at the December meeting, and if some policymakers expect inflation to undershoot the bank’s target, it will justify the debate for further easing at the next meeting.

In the US, the Federal Reserve cut rates by 25 basis points and hinted at a possible pause in its easing cycle, citing a division in the Federal Open Market Committee (FOMC). Also, Fed Chair Jerome Powell revealed the central bank collected state data related to unemployment claims, and noted that the jobs market has not deteriorated as expected.

Daily market movers: Broad US Dollar strength, weighs on the Euro

- The US Dollar Index (DXY), which tracks the performance of the buck versus six currencies, climbs 0.37% to 99.50.

- ECB’s President Lagarde said that she would not complain about the economy expanding by 0.2% in Q3 in the EZ.

- The ECB’s monetary policy statement revealed that inflation is close to 2% and added that it’s not pre-committed to a particular rate path. The ECB noted, “The economy has continued to grow despite the challenging global environment.”

- The Federal Reserve lowered its benchmark rate by 25 basis points to a range of 3.75%–4% in a 10–2 vote. The decision was not unanimous, with Fed Governor Stephen Miran favoring a larger 50-bps cut and Kansas City Fed President Jeffrey Schmid voting to hold rates steady.

- At the press conference, the Fed Chair Jerome Powell surprised the markets, saying “a further reduction in the policy rate at the December meeting is not a foregone conclusion — far from it.”

- Fed Chair Jerome Powell said the central bank’s primary focus remains on the labor market, noting that while official data is limited, state-level unemployment claims suggest the jobs market is not deteriorating sharply.

- Powell also mentioned that several FOMC members view interest rates as either at or near a neutral stance, indicating that monetary policy may be appropriately balanced given current economic conditions.

- Trade news between the US and China boosted the Greenback after President Trump met with his counterpart X Jinping. Trump said the meeting was “amazing,” and that China agreed to resume soybean purchases. Consequently, Washington reduced fentanyl tariffs to 10% and cut tariffs on China’s goods from 57% to 47%. Trump added that rare earths issues were resolved and opened the door to discuss chips with China.

Technical outlook: EUR/USD turned bearish, sellers eye 1.1500

EUR/USD continues to trend downward after falling below 1.1600, with sellers eyeing further downside. Bearish momentum increased as depicted by the Relative Strength Index (RSI), reaching a lower trough.

With that said, the EUR/USD first support would be 1.1550, followed by the October 9 low of 1.1542. A breach of the latter will expose 1.1500 and the August 1 low of 1.1391.

Conversely, if EUR/USD climbs above 1.1600, the pair could consolidate within 1.1600-1.1650, before buyers clear the latter and target the 1.1700 milestone.

Euro FAQs

The Euro is the currency for the 20 European Union countries that belong to the Eurozone. It is the second most heavily traded currency in the world behind the US Dollar. In 2022, it accounted for 31% of all foreign exchange transactions, with an average daily turnover of over $2.2 trillion a day.

EUR/USD is the most heavily traded currency pair in the world, accounting for an estimated 30% off all transactions, followed by EUR/JPY (4%), EUR/GBP (3%) and EUR/AUD (2%).

The European Central Bank (ECB) in Frankfurt, Germany, is the reserve bank for the Eurozone. The ECB sets interest rates and manages monetary policy.

The ECB’s primary mandate is to maintain price stability, which means either controlling inflation or stimulating growth. Its primary tool is the raising or lowering of interest rates. Relatively high interest rates – or the expectation of higher rates – will usually benefit the Euro and vice versa.

The ECB Governing Council makes monetary policy decisions at meetings held eight times a year. Decisions are made by heads of the Eurozone national banks and six permanent members, including the President of the ECB, Christine Lagarde.

Eurozone inflation data, measured by the Harmonized Index of Consumer Prices (HICP), is an important econometric for the Euro. If inflation rises more than expected, especially if above the ECB’s 2% target, it obliges the ECB to raise interest rates to bring it back under control.

Relatively high interest rates compared to its counterparts will usually benefit the Euro, as it makes the region more attractive as a place for global investors to park their money.

Data releases gauge the health of the economy and can impact on the Euro. Indicators such as GDP, Manufacturing and Services PMIs, employment, and consumer sentiment surveys can all influence the direction of the single currency.

A strong economy is good for the Euro. Not only does it attract more foreign investment but it may encourage the ECB to put up interest rates, which will directly strengthen the Euro. Otherwise, if economic data is weak, the Euro is likely to fall.

Economic data for the four largest economies in the euro area (Germany, France, Italy and Spain) are especially significant, as they account for 75% of the Eurozone’s economy.

Another significant data release for the Euro is the Trade Balance. This indicator measures the difference between what a country earns from its exports and what it spends on imports over a given period.

If a country produces highly sought after exports then its currency will gain in value purely from the extra demand created from foreign buyers seeking to purchase these goods. Therefore, a positive net Trade Balance strengthens a currency and vice versa for a negative balance.

XRP extends decline after Fed rate cut, Trump-Xi trade deal

Ripple (XRP) declines alongside crypto majors such as Bitcoin (BTC) and Ethereum (ETH), trading above $2.45 at the time of writing on Thursday. The selling pressure in the broader cryptocurrency market followed the Federal Reserve (Fed) lowering interest rates by 25 basis points to a range of 3.75% to 4.00%.

XRP downside risks surge after Fed Chair Powell’s remarks

Although the rate cut was largely expected, Fed Chair Jerome Powell’s comments following the Federal Open Market Committee (FOMC) meeting on Wednesday spooked markets that had priced in at least three rate cuts this year. Powell’s outlook dampened sentiment across the crypto market, extending the correction since Monday.

“In the committee’s discussions at this meeting, there were strongly differing views about how to proceed in December,” Powell stated. “A further reduction in the policy rate at the December meeting is not a foregone conclusion. Far from it.”

Meanwhile, markets briefly reacted to United States (US) President Donald Trump’s meeting with Chinese President Xi Jinping in South Korea, rising before erasing the gains.

President Trump called the meeting with President Xi “amazing,” announcing several outcomes, including a 10% reduction in tariffs to 47% from the current 57%, the removal of bottlenecks on rare-earth metals, and the resumption of soybean exports to the Asian economic giant, among others.

President Trump said they signed a one-year agreement that will be extended. Trump added President Xi will visit the US next year, while President Trump will head to China in April.

Sentiment in the broader cryptocurrency market appeared to worsen despite the US and China easing trade tensions. XRP remains below $2.50 at the time of writing, with key technical indicators hinting at a continued correction in the short term.

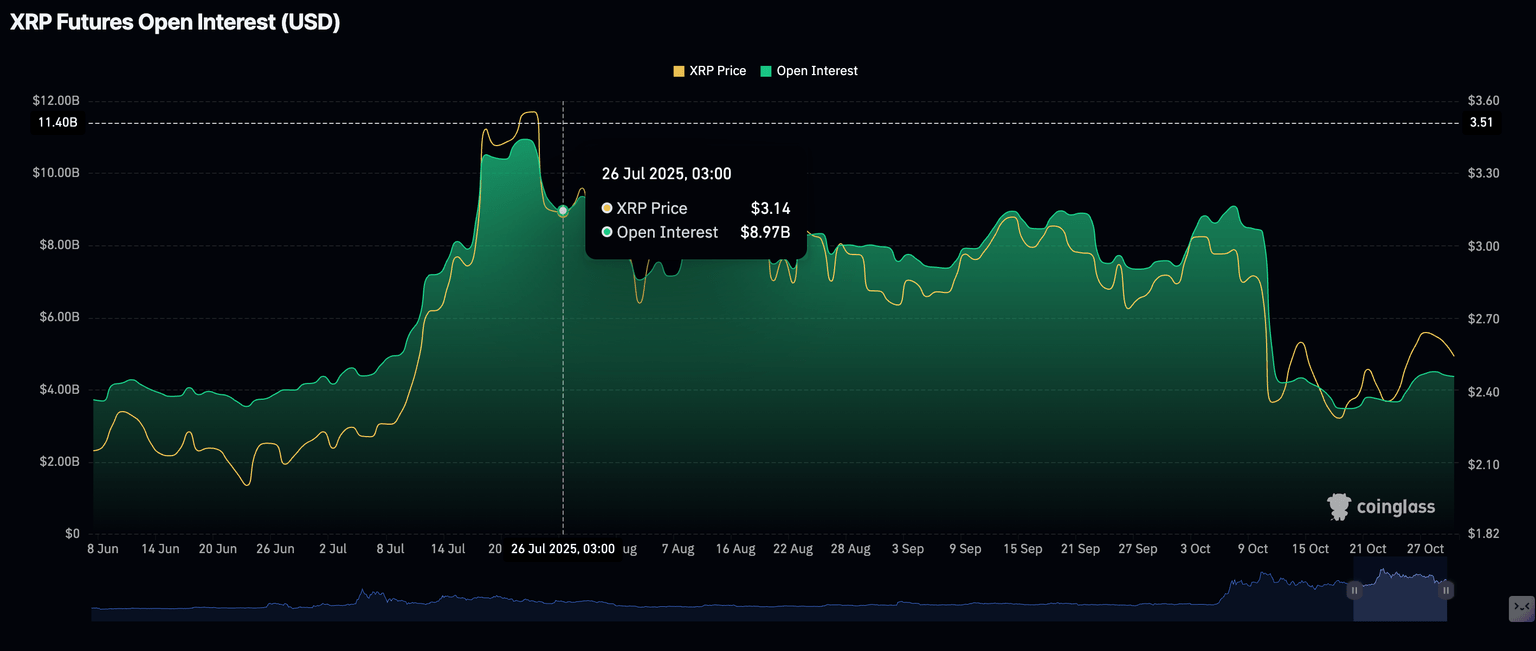

Meanwhile, XRP futures Open Interest (OI) is down approximately 41% to $4.37 billion from $7.43 billion on October 1. Although OI has improved from a monthly low of $3.49 billion, general interest in the token remains significantly suppressed compared to July, when XRP rallied to $3.66, its current record high.

XRP futures Open Interest | Source: CoinGlass

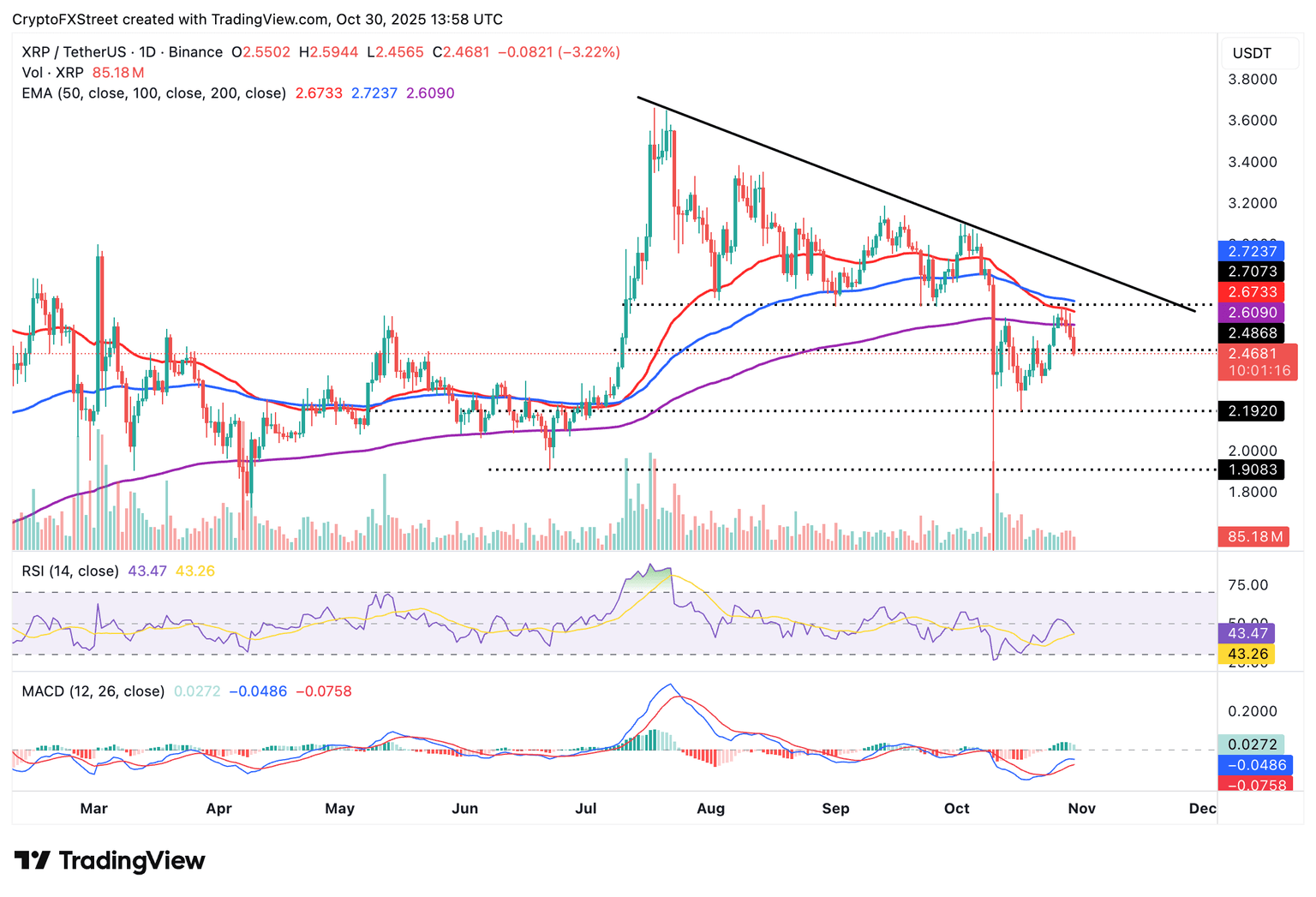

Technical outlook: XRP bears tighten their grip

XRP holds its position below key moving averages, including the 200-day Exponential Moving Average (EMA) at $2.60, the 50-day EMA at $2.67, and the 100-day EMA at $2.72, suggesting a top-heavy technical structure.

The Relative Strength Index (RSI), at 43 and falling, indicates that bearish momentum is increasing, which could accelerate the pullback toward support at $2.18, last tested on October 17.

XRP/USDT daily chart

Still, if investors buy the dip, seeking new entry positions after the drawdown and XRP closes the day above $2.50, a trend reversal could occur. Moreover, the Moving Average Convergence Divergence (MACD) has maintained a buy signal since last Friday, encouraging investors to increase exposure and contributing to buying pressure.

Key milestones traders will watch for include a sustained break above the 200-day EMA at $2.60, the 50-day EMA at $2.67 and the 100-day EMA at $2.72. If bulls push above the trendline resistance on the daily chart, the path of least resistance would remain upward, increasing the odds of a rally toward the record high of $3.66.

Ripple FAQs

European Central Bank expected to keep interest rates unchanged for a third straight meeting

The European Central Bank (ECB) is expected to stand pat for the third consecutive monetary policy meeting, holding the interest rate on the main refinancing operations, the marginal lending facility and the deposit facility at 2.15%, 2.4% and 2%, respectively. The decision will be announced on Thursday at 13:15 GMT.

The interest rate decision will not be accompanied by the staff’s updated economic projections, but will be followed by ECB President Christine Lagarde’s press conference at 13:45 GMT.

The EUR/USD pair will likely experience intense volatility following the ECB’s policy announcements, as Euro (EUR) traders will look for fresh signals on whether the central bank is done with its rate-cutting cycle.

Follow FXStreet’s ECB Live Coverage here

What to expect from the ECB interest rate decision?

During the press conference following the September meeting, ECB President Lagarde highlighted that the “domestic economy is showing resilience.”

While commenting on the inflation outlook, Lagarde said: “The disinflationary process is over. We are still in a good place and inflation is where we want it to be.”

The latest inflation and economic activity data justified her words, with the core Eurozone Harmonized Index of Consumer Prices (HICP) ticking up to an annual rate of 2.4% in September, compared to 2.3% previously, but remaining close to the central bank’s 2% inflation target.

Meanwhile, the bloc’s preliminary October HCOB Composite Purchasing Managers’ Index (PMI) climbed to 52.2, the highest level since May 2024, as both the manufacturing and services sectors performed stronger-than-expected in the reported period.

The preliminary reading of the Eurozone’s third-quarter Gross Domestic Product (GDP) is due for release on Thursday, a few hours before the ECB policy verdict, and is expected to have increased by 0.1% on the quarter, at the same pace seen in the previous period.

Against this backdrop, it seems that ECB President Lagarde and some of her colleagues have set a high bar for further easing, with industry experts and analysts expecting the central bank to be unlikely to reduce rates until March next year.

“The swaps market continues to price in about 50% odds that the ECB delivers one more 25bps cut in the next 12 months and the policy rate to bottom at 1.75%,” analysts at BBH noted.

Previewing the ECB policy announcement, analysts at TD Securities (TDS) said: “While growth is slowing into year-end, there’s no need for President Lagarde to change her tone from September’s decision, reinforcing an ECB that is happy where it is, but ready to act should risks emerge.”

How could the ECB meeting impact EUR/USD?

EUR/USD remains confined within a narrow range below the 1.1650 barrier in the lead up to the ECB showdown, undermined by the recent US Dollar (USD) resurgence.

Additionally, the French political drama somewhat weighs on the Euro (EUR), acting as a headwind for the pair.

Bloomberg reported on Sunday, “French lawmakers didn’t vote on a Socialist proposal for a wealth tax Saturday, delaying a possible compromise in a budget debate that risks toppling the fragile minority government of Prime Minister Sebastien Lecornu.”

In case the ECB Monetary Policy Statement (MPS) or President Lagarde sticks to the bank’s rhetoric of being “in a good place” or explicitly hints that it is done with rate cuts, it could revive the EUR/USD recovery.

On the other hand, EUR/USD could witness a fresh selling wave should the ECB voice concerns about slowing economic growth, suggesting that the door remains ajar for future interest rate cuts.

Dhwani Mehta, Asian Session Lead Analyst at FXStreet, highlights key technical levels for trading EUR/USD following the monetary policy announcement.

“EUR/USD settled below the critical 21-day Simple Moving Average (SMA) at 1.1638 on Wednesday, incurring heavy losses. Meanwhile, the 14-day Relative Strength Index (RSI) indicator stays bearish while below the 50 level. The daily technical setup, therefore, suggests that downside risks will likely persist.”

“A sustained break below the 1.1575 demand area will fuel a fresh sell-off toward the October low of 1.1542. Further south, sellers could find a strong hurdle at the 1.1500 round figure. Conversely, scaling the 21-day SMA barrier will put the confluence zone around 1.1670 back in focus. The 100-day and 50-day SMAs close in near that level. The next topside targets are aligned at the October 17 high of 1.1728, followed by the 1.1800 mark,” Dhwani adds.

Economic Indicator

ECB Press Conference

Following the European Central Bank’s (ECB) economic policy decision, the ECB President gives a press conference regarding monetary policy. The president’s comments may influence the volatility of the Euro (EUR) and determine a short-term positive or negative trend. If the president adopts a hawkish tone it is considered bullish for the EUR, whereas if the tone is dovish the result is usually bearish for the Euro.

Next release: Thu Oct 30, 2025 13:45

Frequency: Irregular

Consensus: –

Previous: –

Source: European Central Bank

ECB FAQs

The European Central Bank (ECB) in Frankfurt, Germany, is the reserve bank for the Eurozone. The ECB sets interest rates and manages monetary policy for the region.

The ECB primary mandate is to maintain price stability, which means keeping inflation at around 2%. Its primary tool for achieving this is by raising or lowering interest rates. Relatively high interest rates will usually result in a stronger Euro and vice versa.

The ECB Governing Council makes monetary policy decisions at meetings held eight times a year. Decisions are made by heads of the Eurozone national banks and six permanent members, including the President of the ECB, Christine Lagarde.

In extreme situations, the European Central Bank can enact a policy tool called Quantitative Easing. QE is the process by which the ECB prints Euros and uses them to buy assets – usually government or corporate bonds – from banks and other financial institutions. QE usually results in a weaker Euro.

QE is a last resort when simply lowering interest rates is unlikely to achieve the objective of price stability. The ECB used it during the Great Financial Crisis in 2009-11, in 2015 when inflation remained stubbornly low, as well as during the covid pandemic.

Quantitative tightening (QT) is the reverse of QE. It is undertaken after QE when an economic recovery is underway and inflation starts rising. Whilst in QE the European Central Bank (ECB) purchases government and corporate bonds from financial institutions to provide them with liquidity, in QT the ECB stops buying more bonds, and stops reinvesting the principal maturing on the bonds it already holds. It is usually positive (or bullish) for the Euro.

Austria Producer Price Index (MoM): -0.1% (September) vs -0.3%

Gold attracts some buyers during the Asian session on Thursday and now seems to have snapped a four-day losing streak. The US Dollar struggles to capitalize on the previous day’s post-FOMC gains to an over two-week high and drifts lower amid concerns about economic risks stemming from a prolonged US government shutdown.

Japanese Yen weakens after BoJ leaves rates unchanged; focus shifts to post-meeting presser

The Japanese Yen (JPY) edges higher during the Asian session on Thursday, though the upside potential seems limited as traders keenly await the Bank of Japan (BoJ) policy update. Traders will look for cues about the possibility of a rate hike in December or early next year amid speculations that Japan’s new Prime Minister Sanae Takaichi will pursue aggressive fiscal spending plans and resist early tightening. Hence, the outlook will play a key role in determining the next leg of a directional move.

Heading into the key central bank event, the market anxiety ahead of the crucial meeting between US President Donald Trump and his counterpart, Xi Jinping, is seen underpinning the safe-haven JPY amid intervention fears. The US Dollar (USD), on the other hand, struggles to capitalize on Wednesday’s hawkish FOMC-inspired gains to an over two-week high. This keeps a lid on the USD/JPY pair’s solid recovery from the vicinity of mid-151.00s, or a one-week low, touched the previous day.

Japanese Yen benefits from reviving safe-haven demand as traders keenly await the BoJ decision

- The Bank of Japan is widely expected to keep interest rates steady at the end of a two-day policy meeting on Thursday amid the uncertainty over the impact of US trade tariffs and Japan’s new Prime Minister Sanae Takaichi’s pro-stimulus stance.

- Meanwhile, US Treasury Secretary Scott Bessent on Wednesday urged Japan’s government to allow the BoJ space to avoid excess exchange rate volatility, suggesting that the US may keep pressuring Japan to tighten monetary policy more quickly.

- Hence, the market focus will remain glued to the BoJ’s communication on the future pace of rate hikes, which will influence the near-term trajectory for the Japanese Yen. In the meantime, reviving safe-haven demand is seen benefiting the JPY.

- US President Donald Trump will meet Chinese leader Xi Jinping after months of turmoil over trade issues between the world’s two largest economies. This, in turn, keeps investors on the edge and underpins the JPY during the Asian session.

- The US Dollar shot to an over two-week top on Wednesday after the Federal Reserve pushed back against market expectations for another interest rate cut in December. Earlier, the US central bank lowered borrowing costs by 25 basis points.

- The US central bank also said it would stop reducing the size of its balance sheet as soon as December, marking the end of its quantitative tightening. Moreover, economic risks stemming from the US government shutdown weigh on the USD.

USD/JPY mixed technical setup warrants some caution before placing aggressive bearish bets

The USD/JPY pair struggles to find acceptance above the 153.00 mark and remains below the 153.25-153.30 supply zone, or the monthly peak retested earlier this week. The subsequent fall favors bearish traders, though positive oscillators on the daily chart back the case for the emergence of dip-buyers near the 152.00 round figure. A convincing break below the said handle would expose the overnight swing low, around the 151.55-151.50 region, before spot prices extend the slide further towards the 151.10-151.00 pivotal support. Some follow-through selling would confirm a fresh breakdown and pave the way for deeper losses.

On the flip side, the 153.00 round figure now seems to act as an immediate hurdle ahead of the 153.25-153.30 region, above which the USD/JPY pair could aim to reclaim the 154.00 mark. The momentum could extend further towards the next relevant resistance near mid-154.00s en route to the 154.75-154.80 region and the 155.00 psychological mark.

Economic Indicator

BoJ Interest Rate Decision

The Bank of Japan (BoJ) announces its interest rate decision after each of the Bank’s eight scheduled annual meetings. Generally, if the BoJ is hawkish about the inflationary outlook of the economy and raises interest rates it is bullish for the Japanese Yen (JPY). Likewise, if the BoJ has a dovish view on the Japanese economy and keeps interest rates unchanged, or cuts them, it is usually bearish for JPY.

Next release: Thu Oct 30, 2025 03:00

Frequency: Irregular

Consensus: 0.5%

Previous: 0.5%

Source: Bank of Japan