Statistics Canada handed the headline writers a gift and the analysts a headache. Real GDP shrank 0.1% on an annualized basis in the first quarter, and with the fourth quarter of 2025 revised down to a 1.0% contraction, that is two negative quarters in a row, the textbook definition of a technical recession and Canada’s first since the pandemic.

Japan’s Katayama says always ready to react suitably as needed on forex

Japan’s Finance Minister Satsuki Katayama said on Friday that the authorities are always ready to react suitably as needed on foreign exchange.

Meanwhile, Japanese Prime Minister Sanae Takaichi stated that weak Japanese Yen (JPY) has both advantages and disadvantages. She added that the economic policy aims to strengthen Japan’s economic capacity and not to manipulate currency.

Key quotes

Will act if currency volatility rises, inflation pressures deepen.

Declines to comment on currency levels.

Always ready to react suitably as needed on forex.

Middle East conflict and oil price shifts also weigh on weak yen.

Markets highly volatile since strait of Hormuz effectively closed.

Joint statement with US enables decisive action on currency when needed.

FX volatility very high with speculative trades driving major yen shifts since Iran war began in February.

Market reaction

As of writing, the USD/JPY pair is down 0.02% on the day at 160.00.

Japanese Yen FAQs

The Japanese Yen (JPY) is one of the world’s most traded currencies. Its value is broadly determined by the performance of the Japanese economy, but more specifically by the Bank of Japan’s policy, the differential between Japanese and US bond yields, or risk sentiment among traders, among other factors.

One of the Bank of Japan’s mandates is currency control, so its moves are key for the Yen. The BoJ has directly intervened in currency markets sometimes, generally to lower the value of the Yen, although it refrains from doing it often due to political concerns of its main trading partners. The BoJ ultra-loose monetary policy between 2013 and 2024 caused the Yen to depreciate against its main currency peers due to an increasing policy divergence between the Bank of Japan and other main central banks. More recently, the gradually unwinding of this ultra-loose policy has given some support to the Yen.

Over the last decade, the BoJ’s stance of sticking to ultra-loose monetary policy has led to a widening policy divergence with other central banks, particularly with the US Federal Reserve. This supported a widening of the differential between the 10-year US and Japanese bonds, which favored the US Dollar against the Japanese Yen. The BoJ decision in 2024 to gradually abandon the ultra-loose policy, coupled with interest-rate cuts in other major central banks, is narrowing this differential.

The Japanese Yen is often seen as a safe-haven investment. This means that in times of market stress, investors are more likely to put their money in the Japanese currency due to its supposed reliability and stability. Turbulent times are likely to strengthen the Yen’s value against other currencies seen as more risky to invest in.

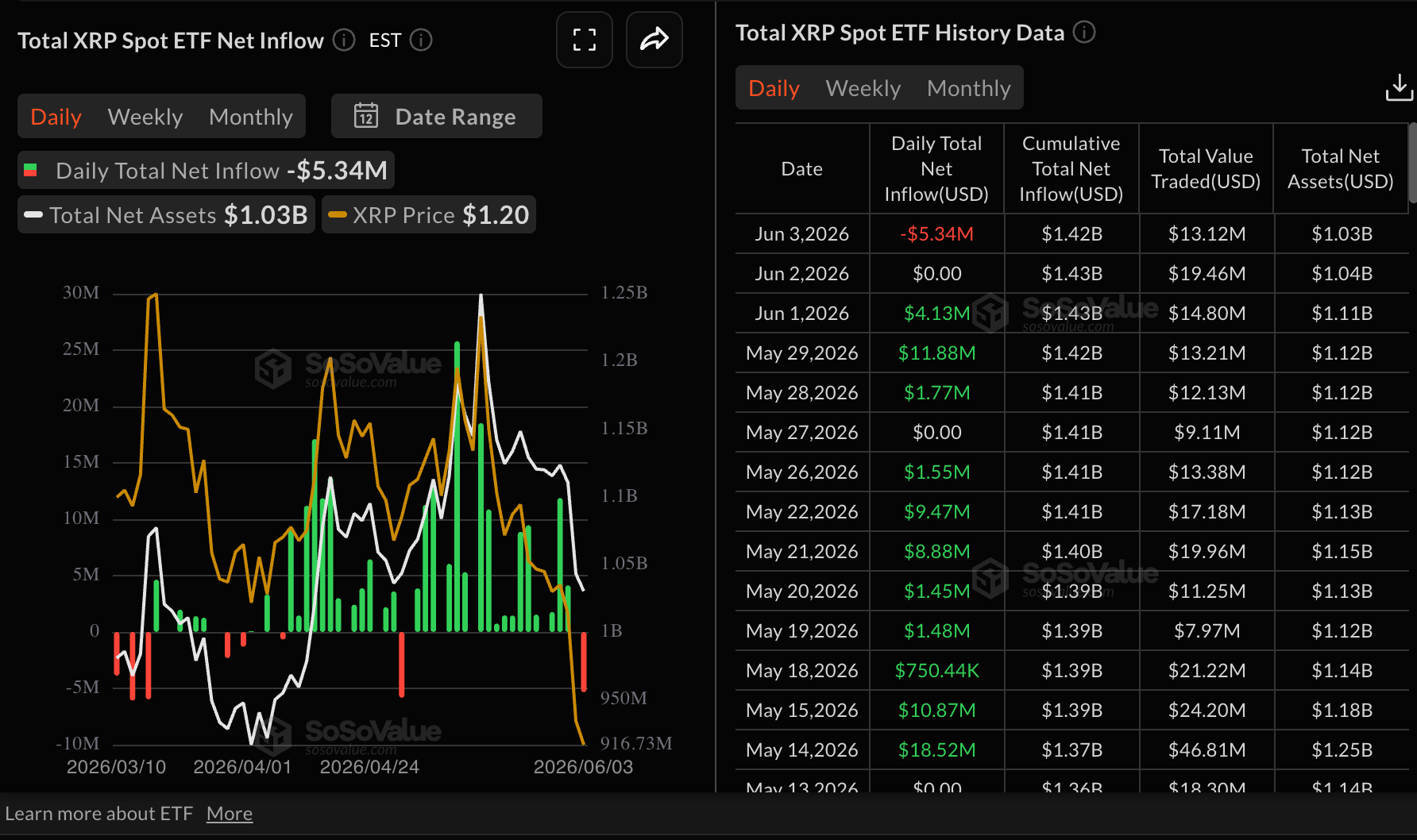

XRP slumps toward $1.00 as ETF outflows, weak technicals fuel bearish outlook

Ripple (XRP) edges lower, trading around $1.15 at the time of writing on Thursday, its lowest price since February 6. The cross-border money remittance token is extending the sell-off for the fifth consecutive day, reflecting persistent headwinds from ongoing geopolitical tensions and investor uncertainty.

XRP ETF outflows reinforce bearish outlook

Institutional interest in XRP spot Exchange-Traded Funds (ETFs) took a negative turn, with roughly $5 million in outflows on Wednesday. According to SoSoValue data, this marks the first outflow since April 30.

Cumulative inflows into XRP investment products stand at $1.42 billion, while average assets under management hover around $1.03 billion, underscoring sustained institutional interest despite recent market volatility.

Should risk aversion continue and institutional investors further trim their exposure, increased supply pressure could accelerate XRP’s decline below the tentative $1.00 support level.

“Tensions between the United States and Iran continue to generate concern across global financial markets, triggering recurring episodes of risk aversion,” Simon-Peter Massabni, Head of Business Development at XS.com, said in a written statement. “In such environments, investors typically reduce exposure to more volatile assets, such as cryptocurrencies, while favoring more defensive positions,” he added.

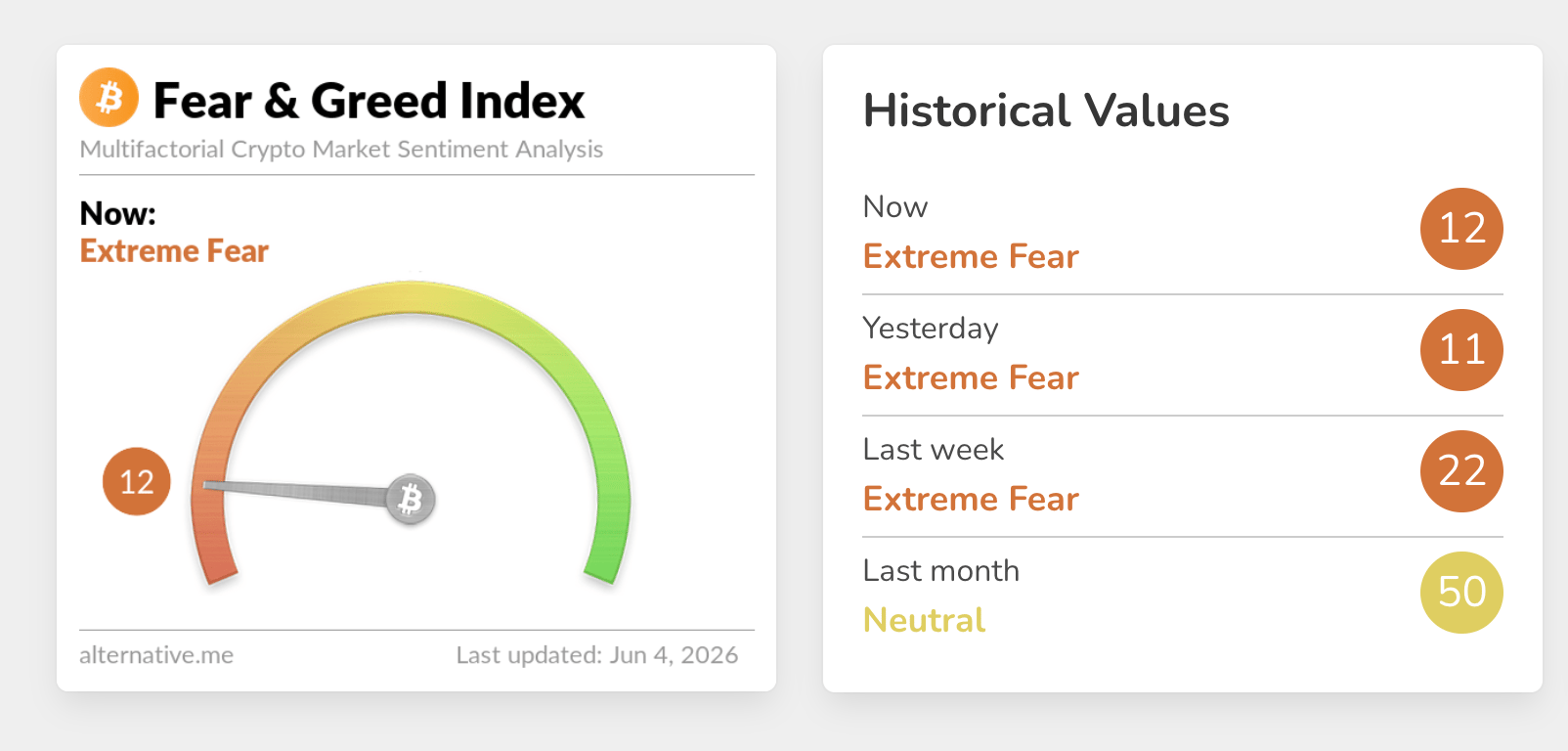

Sentiment across the crypto market remains significantly subdued, as reflected in the Fear & Greed Index, holding at 12 in Extreme Fear territory on Thursday, down from 50 in May.

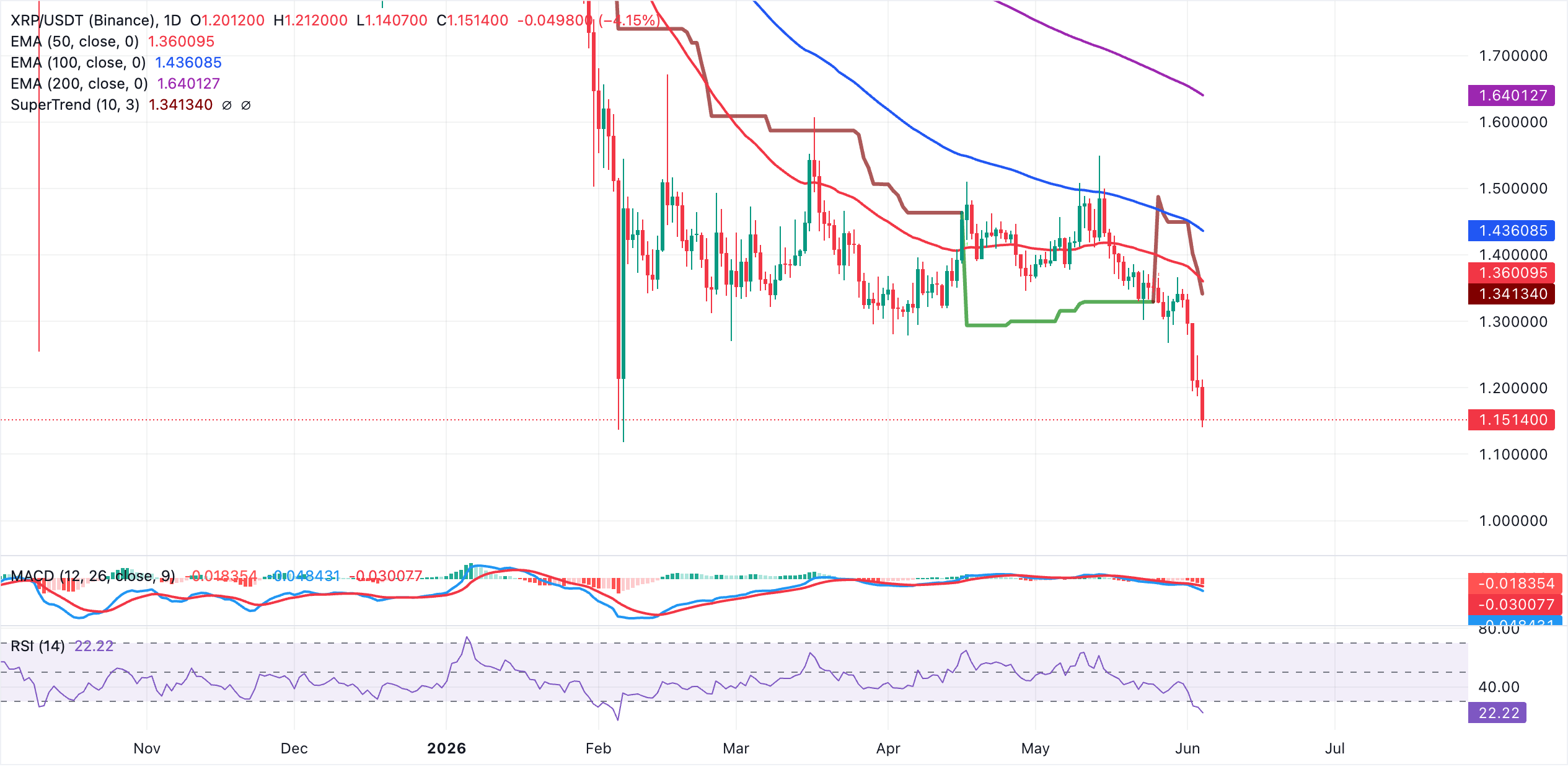

Price analysis: XRP stuck in a persistent drawdown

XRP trades at $1.15, holding well below the 50-day, 100-day and 200-day Exponential Moving Averages (EMAs), keeping the near-term bias bearish as rallies struggle against a dense band of overhead supply.

The SuperTrend line at $1.34 also sits above spot, reinforcing a downside-skewed structure, while the Relative Strength Index (RSI) near 22 on the daily chart suggests deeply oversold conditions that may slow, but not yet reverse, the prevailing downtrend, especially with the Moving Average Convergence Divergence (MACD) histogram in negative territory.

On the topside, initial resistance is seen at the SuperTrend barrier around $1.34, with the 50-day EMA nearby at $1.36 forming the next cap if a corrective bounce materializes. Further up, the 100-day EMA at roughly $1.44 and the more distant 200-day EMA near $1.64 outline subsequent resistance tiers that would need to be reclaimed to ease the broader bearish pressure.

(The technical analysis of this story was written with the help of an AI tool.)

Cryptocurrency metrics FAQs

Oil: Middle East conflict reshapes outlook – BNY

Bob Savage highlights that the OECD now sees the Middle East conflict as the main driver of the global outlook, with surging energy and input prices lifting inflation and weighing on growth. The OECD cut its 2026 global GDP forecast and outlines time-limited versus prolonged disruption scenarios, warning inflation could rise notably under a prolonged shock while urging central banks to stay vigilant.

OECD warns on energy-driven risks

“The OECD has warned that the Middle East conflict has become the main driver of the global outlook, with energy and input prices surging since February, lifting inflation while weighing on real incomes and growth.”

“It cut its projected global GDP growth for 2026 to 2.8% from 3.4%, while leaving 2027 unchanged at 3.1%.”

“Its outlook presents two scenarios: a time-limited disruption, where growth slows modestly before recovering, and a prolonged disruption, where higher energy prices, supply shortages, tighter financial conditions and weaker confidence would depress activity further.”

“Inflation could rise by around 0.4 percentage points in 2026 and 1.3 percentage points in 2027 under the prolonged scenario.”

“The OECD is urging central banks to remain vigilant where temporarily higher headline inflation resulting from the energy price shock can be looked through provided longer-term inflation expectations remain well-anchored, and says governments should keep energy relief temporary, targeted and well-designed.”

(This article was created with the help of an Artificial Intelligence tool and reviewed by an editor.)

Euro bounces up against the US Dollar despite weak Eurozone Retail Sales data

The Euro (EUR) is rallying against a weaker US Dollar (USD) in Thursday’s European trading session, reversing Wednesday’s losses and returning to the 1.3630 area at the time of writing. A moderate improvement in market sentiment following news of a ceasefire in Lebanon has offset the weak Eurozone Retail Sales report released earlier in the day.

The safe-haven US Dollar is struggling on Thursday, following reports of an agreement between Israel and Lebanon to implement the ceasefire, which is pending confirmation by Hezbollah. This agreement is seen as the first step to disentangle the stalemate in Iran and advance towards a durable peace in the region.

A moderate market optimism is keeping the safe-haven US Dollar under pressure and buoying the Euro, which has been unfazed by a 0.4% decline in Eurozone Retail Sales in April. The final data overshoots market expectations of a 0.3% drop, although the upward revision of March’s figures –to a 0.8% increase from the 0.1% drop previously estimated– has contributed to cushioning the negative impact on the common currency.

Technical Analysis: The Euro keeps wavering within range

The broader technical picture, however, remains little changed. The EUR/USD trades at 1.1631, holding in a broadly neutral stance with price action trapped within the last two and a half weeks’ trading range, between 1.1570 and 1.1660.

Technical indicators in 4-hour charts are mixed, endorsing the neutral view. The Relative Strength Index (RSI) is right above the 50 midline, while the Moving Average Convergence Divergence (MACD) remains slightly negative.

Upside attempts are likely to find significant resistance at the 1.1660 area, which has been capping bulls since mid-May. Above that level, the next targets are the May 14 high, at 1.1720, and May’s peak, in the 1.1790 area.

On the downside, the 1.1600 round level has contained bears this week, guarding the path towards the range bottom, at the 1.1570 level (May 21 low). A confirmation below this level would put April’s bottom at the 1.1505-1.1525 on the bears’ focus.

(The technical analysis of this story was written with the help of an AI tool.)

Economic Indicator

Retail Sales (MoM)

The Retail Sales data, released by Eurostat on a monthly basis, measures the volume of retail sales in the Eurozone. It shows the performance of the retail sector in the short term, which accounts for around 5% of the total value added of the Eurozone economies. Retail Sales data is widely followed as an indicator of consumer spending. Percent changes reflect the rate of changes in such sales, with the MoM reading comparing sales volumes in the reference month with the prior month. Generally, a high reading is seen as bullish for the Euro (EUR), while a low reading is seen as bearish

Last release: Thu Jun 04, 2026 09:00

Frequency: Monthly

Actual: -0.4%

Consensus: -0.3%

Previous: -0.1%

Source: Eurostat

Economic Indicator

Retail Sales (YoY)

The Retail Sales data, released by Eurostat on a monthly basis, measures the volume of retail sales in the Eurozone. It shows the performance of the retail sector in the short term, which accounts for around 5% of the total value added of the Eurozone economies. Retail Sales data is widely followed as an indicator of consumer spending. Percent changes reflect the rate of changes in such sales, with the YoY reading comparing sales volumes in the reference month with the same month a year earlier. Generally, a high reading is seen as bullish for the Euro (EUR), while a low reading is seen as bearish.

Last release: Thu Jun 04, 2026 09:00

Frequency: Monthly

Actual: 1%

Consensus: 0.3%

Previous: 1.2%

Source: Eurostat

Switzerland Consumer Price Index (YoY) came in at 0.6% below forecasts (0.8%) in May

Statistics Canada handed the headline writers a gift and the analysts a headache. Real GDP shrank 0.1% on an annualized basis in the first quarter, and with the fourth quarter of 2025 revised down to a 1.0% contraction, that is two negative quarters in a row, the textbook definition of a technical recession and Canada’s first since the pandemic.

British Pound edges higher vs softer USD; lacks bullish conviction as Iran risks persist

The GBP/USD pair attracts some dip-buyers following the previous day’s slide back closer to the weekly low and trades above the 1.3400 mark during the Asian session on Thursday. The uptick is sponsored by a softer US Dollar (USD), though the upside potential seems limited amid persistent geopolitical uncertainties.

In a joint statement with the US on Wednesday, Israel and Lebanon announced they agreed to the implementation of a ceasefire after peace talks in Washington. The latest development eases concerns about a broader regional conflict and keeps a lid on the safe-haven USD’s move higher witnessed since the beginning of this week. This, in turn, is seen as a key factor offering some support to the GBP/USD pair. However, renewed hostilities in the Gulf keep geopolitical risks in play and should limit deeper USD losses, warranting caution before placing aggressive bullish bets on the currency pair.

The US military said on Tuesday that it had successfully repelled multiple Iranian missiles and drones launched at Kuwait and Bahrain, and had conducted self-defense strikes on Qeshm Island in response to the attacks. Meanwhile, Iranian armed forces targeted the US military bases in Bahrain in retaliation for the strike on Qeshm. This comes on the back of the lack of a progress in US-Iran diplomatic negotiations, amid a standoff over Tehran’s nuclear program and the Strait of Hormuz. Furthermore, bets that the US Federal Reserve (Fed) will hike rates in 2026 should support the buck and cap the GBP/USD pair.

Traders might also opt to move to the sidelines ahead of the release of the closely watched US monthly employment details, popularly known as the Nonfarm Payrolls (NFP) report, on Friday. The crucial jobs data will be looked for more cues about the Fed’s future policy path. This, along with further developments surrounding the Middle East crisis, should infuse volatility across global financial markets and influence USD price dynamics. Nevertheless, the fundamental backdrop seems tilted in favor of USD bulls, suggesting that the GBP/USD pair is likely to attract fresh sellers at higher levels.

Pound Sterling FAQs

The Pound Sterling (GBP) is the oldest currency in the world (886 AD) and the official currency of the United Kingdom. It is the fourth most traded unit for foreign exchange (FX) in the world, accounting for 12% of all transactions, averaging $630 billion a day, according to 2022 data.

Its key trading pairs are GBP/USD, also known as ‘Cable’, which accounts for 11% of FX, GBP/JPY, or the ‘Dragon’ as it is known by traders (3%), and EUR/GBP (2%). The Pound Sterling is issued by the Bank of England (BoE).

The single most important factor influencing the value of the Pound Sterling is monetary policy decided by the Bank of England. The BoE bases its decisions on whether it has achieved its primary goal of “price stability” – a steady inflation rate of around 2%. Its primary tool for achieving this is the adjustment of interest rates.

When inflation is too high, the BoE will try to rein it in by raising interest rates, making it more expensive for people and businesses to access credit. This is generally positive for GBP, as higher interest rates make the UK a more attractive place for global investors to park their money.

When inflation falls too low it is a sign economic growth is slowing. In this scenario, the BoE will consider lowering interest rates to cheapen credit so businesses will borrow more to invest in growth-generating projects.

Data releases gauge the health of the economy and can impact the value of the Pound Sterling. Indicators such as GDP, Manufacturing and Services PMIs, and employment can all influence the direction of the GBP.

A strong economy is good for Sterling. Not only does it attract more foreign investment but it may encourage the BoE to put up interest rates, which will directly strengthen GBP. Otherwise, if economic data is weak, the Pound Sterling is likely to fall.

Another significant data release for the Pound Sterling is the Trade Balance. This indicator measures the difference between what a country earns from its exports and what it spends on imports over a given period.

If a country produces highly sought-after exports, its currency will benefit purely from the extra demand created from foreign buyers seeking to purchase these goods. Therefore, a positive net Trade Balance strengthens a currency and vice versa for a negative balance.

New Zealand Dollar plunges as hawkish Fed remarks boost US Dollar

The NZD/USD pair trades near the 0.5860 region on Thursday, down more than 1% in the day, as the US Dollar (USD) strengthens following hawkish remarks from Federal Reserve (Fed) officials.

Federal Reserve Bank of Dallas President Lorie Logan stated that inflation is taking too long to return to the Fed’s 2% target and warned that higher interest rates could be necessary later this year.

Logan added that financial conditions remain accommodative, the labor market is stable, and economic activity continues to show resilience, reinforcing expectations that the Fed may maintain a restrictive policy stance for longer.

The Greenback also remained supported after the latest ISM Services PMI rose to 54.5 in May from 53.6 in April, highlighting the resilience of the US economy and reducing expectations for near-term interest rate cuts.

Meanwhile, investors remain focused on Friday’s US Nonfarm Payrolls report for additional clues on the strength of the labor market and the Fed’s policy outlook.

Short-term technical analysis:

On the 4-hour chart, NZD/USD trades at 0.5864, maintaining a capped tone as the pair remains below the 100-period Simple Moving Average (SMA) at 0.5892 and the 20-period SMA at 0.5929. The recent slide has driven the Relative Strength Index (RSI) into oversold territory near 27, hinting that bearish pressure dominates for now, even as the risk of a corrective bounce from depressed momentum levels starts to rise.

On the topside, immediate resistance emerges at 0.5866, with additional barriers clustered at 0.5870 and 0.5880, ahead of the 100-period SMA at 0.5892 and the more distant 20-period SMA near 0.5929. On the downside, initial support is seen at 0.5857, where a horizontal level underpins the pair, and a break below this floor would open the door to further weakness despite the already oversold momentum backdrop.

(The technical analysis of this story was written with the help of an AI tool.)

Indonesian Rupiah: State-led commodity shift reshapes risks – MUFG

MUFG’s Lloyd Chan highlights that Indonesia is undergoing a structural regime shift as the state moves toward direct control of key commodity exports via Danantara Sumberdaya Indonesia. The report stresses high near-term implementation risks for the Rupiah, but notes that over the medium term, effective execution could bolster external stability while poor execution could weigh on the currency.

State control raises Rupiah risk profile

“A structural regime shift is underway. Indonesia is transitioning toward a state-controlled commodity export system under Danantara Sumberdaya Indonesia (DSI), a new subsidiary of the Danantara sovereign wealth fund. Unlike global precedents typically focused on a single commodity resource, Indonesia is attempting to apply this model across multiple key commodities such as coal, palm oil, and ferroalloys, making the scope both unique and execution intensive.”

“Implementation risks are high in the near term. Uncertainty during the rollout phase could disrupt trade flows, create pricing ambiguity, and weigh on investor sentiment. Markets appear to be pricing this risk, with the rupiah underperforming regional peers amid a softening macro backdrop – including a sharply narrowing trade surplus ($89mn in April vs. $3.3bn in March), declining FX reserves (down ~USD6.3bn YoY in April), and persistent capital outflows.”

“We expect the government to take direct control of several key commodity exports. Market mechanisms are not eliminated, but increasingly mediated by the state. Prices could still reference global benchmarks, even as state influence rises.”

“USD/IDR could develop a mild downside bias on an unwinding of crowded long USD/IDR positioning and cheap valuations. US–Iran de-escalation could be a key trigger for reversal.”

“Policy outcomes are inherently binary over the medium term. Effective execution would strengthen Indonesia’s external position and underpin rupiah stability, while poor execution or policy overreach risks disrupting trade flows, eroding competitiveness, and driving prolonged currency weakness.”

“BI’s policy support will help to partially offset rising country risk premia. The central bank has raised policy rate by 50bps in May and enhanced FX support measures via issuing more high-yielding SRBI, helping to improve the rupiah’s front-end carry appeal.”

(This article was created with the help of an Artificial Intelligence tool and reviewed by an editor.)

Canada Labor Productivity (QoQ) came in at -0.5% below forecasts (0.7%) in 1Q

The Japanese Yen bounced up from five-week lows against the US Dollar, turning positive on the daily chart, as Japan’s Prime Minister Sanae Takaichi warned that Tokyo is ready to take action against Yen weakness. The USD/JPY pair has pulled back from the 160.00 level, considered a line in the sand for Japanese authorities, to hit session lows at 159.55.